Other Personal Finance Tools

Once you open all five accounts, you can use free online tools, like those listed below, to monitor your monthly budget, net worth, and investment performance across each account all in one place.

Net Worth and Investment Tracker

It’s hard to monitor your money across different accounts. To help you have better visibility over your finances, we recommend using a free online personal finance tool called Personal Capital.

It helps you track your budget, spending, net worth, investment portfolio, and investment allocation all in one place.

Want to learn more? Here is our review of Personal Capital.

Recommended Next Steps

- If you don’t have Personal Capital, sign up today.

Budgeting Tool

Tracking your expenses sucks. We’re not going to sugarcoat it. However, it’s essential that you do it.

Mint.com provides the best automatic way to understand how much you spend across different categories. A few years ago, we weren’t a fan of them, but they completely revamped their tech and it’s solid now.

Mint will give you visibility into exactly how much you spend each month and enable you to input numbers into your monthly plan in a much simpler and faster way.

Most importantly, it will help you be accurate when you identify how much money you have left to save and invest each month.

Want to learn more? We break down both tools in our post Personal Capital vs Mint.

Recommended Next Steps

- If you don’t have Mint, sign up today.

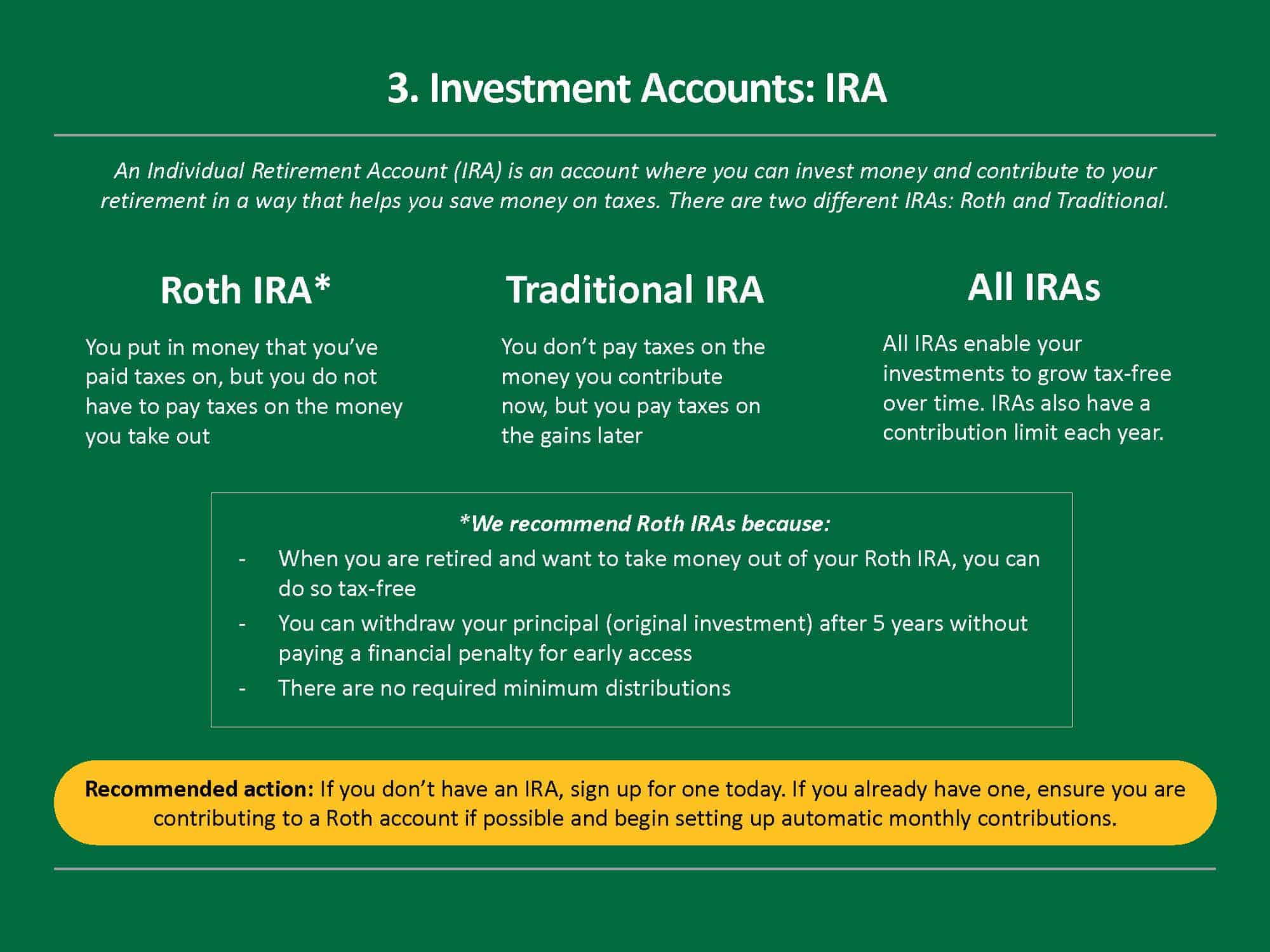

Summary of Accounts

This table is a summary of each account type and what we recommend.

|

Account Type |

Account |

Recommended Accounts |

|

Essential Accounts |

Checking account (aka bank account) |

|

|

Online high yield savings account |

|

|

|

Investment Accounts |

Roth or traditional IRA (Individual Retirement Account) |

|

|

401(k) Retirement Account or 403(b) Retirement Account |

|

|

|

Brokerage account |

|

|

|

Free Financial Management Tools |

Best Free Budgeting Tool |

|

|

Best Free Net Worth and Investment Monitoring Tool |

| Note: If you don’t want a bunch of different accounts and would rather have everything in one place, you can open a checking, high yield savings, IRA and brokerage account with Betterment (4 out of 5 accounts in one place). |

It’s nearly impossible to find educated people in this particular subject, however, you seem like you know what you’re talking about! Thanks